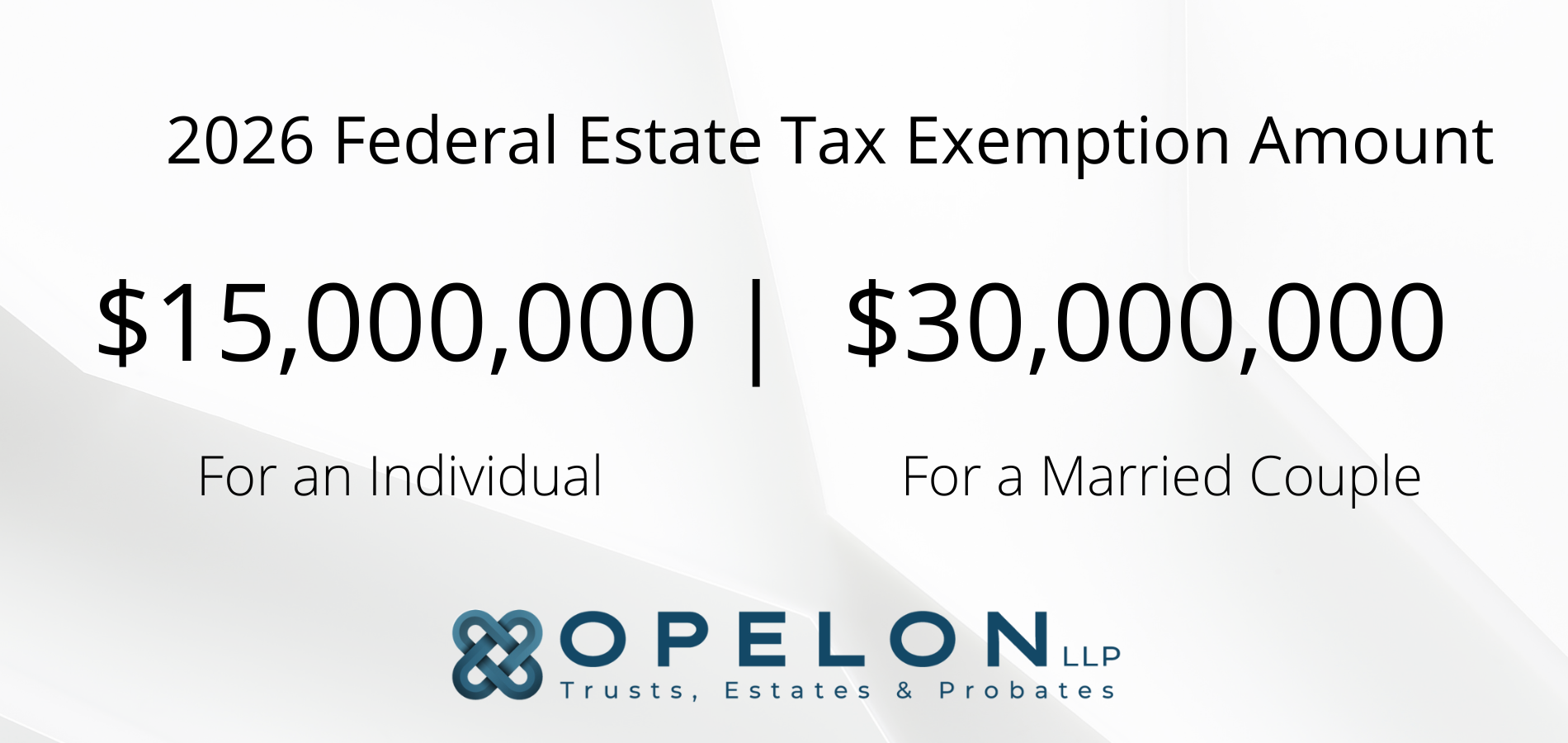

The 2026 federal estate tax exemption is $15 million per individual and $30 million per married couple. The One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, made this amount permanent. The exemption is indexed for inflation starting in 2027. The $30 million couple figure is available only through portability or proper credit shelter trust planning, not automatically.

California has no state estate tax. For most California families, only the federal exemption applies.

If your estate is approaching or above the federal exemption, see our California Estate Tax Planning Guide for High-Net-Worth Families for detailed planning strategies.

Key Takeaways for the 2026 Federal Estate Tax Exemption

- 2026 exemption: $15 million per individual, $30 million per married couple with timely portability election or credit shelter planning.

- Permanent under OBBBA, signed July 4, 2025. Indexed for inflation starting 2027.

- California has no state estate tax or inheritance tax.

- Federal estate tax rate above the exemption: 40% (IRC §2001).

- Annual gift tax exclusion for 2026: $19,000 per recipient (IRC §2503(b)).

- Most California families will not owe federal estate tax.

- Probate avoidance through a living trust remains valuable for most California homeowners, particularly given home values that typically exceed the $750,000 threshold for the simplified petition under Probate Code §13150.

2026 Federal Estate and Gift Tax Summary

This table shows the key federal estate and gift tax figures for 2026.

Tax or Threshold | 2026 Amount | Authority |

Federal estate tax exemption (individual) | $15,000,000 | IRC §2010(c), OBBBA |

Federal estate tax exemption (married couple, with portability) | $30,000,000 | IRC §2010(c), OBBBA |

GST tax exemption (individual) | $15,000,000 | IRC §2631, OBBBA |

Annual gift tax exclusion (per recipient) | $19,000 | IRC §2503(b) |

Married couple combined annual exclusion (gift splitting) | $38,000 | IRC §2513 |

Federal estate tax rate above exemption | Up to 40% | IRC §2001 |

California state estate tax | None | Inheritance tax repealed 1982; pickup estate tax inoperative 2005 |

How the Federal Estate Tax Exemption Works

The federal estate tax applies only when a person dies with assets above the exemption amount. Estates below the threshold owe no federal estate tax.

Estate value is determined by the fair market value of assets at death. This includes real estate, financial accounts, retirement accounts, life insurance proceeds (if owned by the decedent), business interests, and personal property.

Lifetime gifts above the annual exclusion ($19,000 per recipient in 2026) reduce the lifetime exemption on a dollar-for-dollar basis. The estate and gift tax systems are unified under IRC §2010. For deeper coverage of HNW planning strategies, see our California Estate Tax Planning Guide.

Gift Tax and Portability (Brief)

Annual Gift Tax Exclusion

The annual exclusion is $19,000 per recipient for 2026 (IRC §2503(b)). A married couple can split gifts under IRC §2513 to give $38,000 per recipient per year.

Direct payments for tuition and qualified medical expenses are unlimited and not counted against the annual exclusion (IRC §2503(e)). Pay these amounts directly to the school or provider, not to the beneficiary.

Portability and the DSUE

Portability under IRC §2010(c) lets a surviving spouse use the deceased spouse’s unused exclusion amount, called the DSUE. This effectively gives married couples a combined $30 million federal exemption in 2026, but only if the election is properly made.

Claiming portability requires filing IRS Form 706 at the first death, even if no estate tax is due. The standard deadline is nine months after the date of death, with an automatic six-month extension available. Executors of estates not otherwise required to file Form 706 may elect portability up to five years after the decedent’s date of death under Rev. Proc. 2022-32. Portability is not available for the GST tax exemption.

For complete coverage of gift tax planning, portability strategy, and the trade-offs against using a bypass trust, see the California Estate Tax Planning Guide.

California Has No State Estate Tax

California has no state estate tax and no inheritance tax. Voters repealed the California inheritance and gift taxes in 1982 through Proposition 6, which also created a pickup estate tax tied to the federal state death tax credit. That pickup tax became inoperative for decedents dying on or after January 1, 2005, when the federal credit was fully replaced by a deduction. No state-level death tax has been enacted since.

State | State Estate Tax Exemption |

California | None (no state estate or inheritance tax) |

Oregon | $1 million |

Massachusetts | $2 million |

Washington | $3.076 million (deaths 1/1/26 through 6/30/26); $3 million (deaths on or after 7/1/26) |

New York | $7.35 million |

Hawaii | $5.49 million |

Other California taxes still affect estates. Proposition 19 reassessment can apply to inherited real estate, and capital gains may apply to highly appreciated assets sold after death. The California Estate Tax Planning Guide covers these issues in detail.

When You Need More Than the Exemption Number

Knowing the exemption number is the starting point. The following situations require strategic planning beyond a basic figure:

- Your individual estate is approaching $13 million, or your couple estate is approaching $30 million.

- Your assets include significant appreciation potential (real estate, equity, private business interests).

- You own a business, a real estate portfolio, or concentrated investment positions.

- You have charitable goals or a non-citizen spouse.

- You want to protect generational wealth from future estate, gift, or GST tax exposure.

Our California Estate Tax Planning Guide for High-Net-Worth Families covers SLATs, GRATs, ILITs, charitable trusts, generation-skipping trusts, and other strategies in depth. To discuss your situation, call our Carlsbad office at (760) 278-1116.

Frequently Asked Questions about the 2026 federal estate tax exemption

The 2026 federal estate tax exemption is $15 million per individual and $30 million per married couple with portability under IRC §2010(c). The exemption is permanent under OBBBA, signed July 4, 2025, and is indexed for inflation starting 2027. The federal estate tax rate above the exemption is up to 40%.

No. The TCJA-era sunset that would have cut the exemption roughly in half on January 1, 2026, was eliminated by the One Big Beautiful Bill Act. The $15 million per-individual exemption is now permanent, with inflation adjustments starting in 2027.

No. California has no state estate tax and no inheritance tax. The California inheritance tax was repealed by Proposition 6 in 1982, and the pickup estate tax that replaced it became inoperative in 2005 when the federal state death tax credit was eliminated. Only the federal estate tax applies to California estates, and only for estates above $15 million per individual.

The 2026 annual gift tax exclusion is $19,000 per recipient (IRC §2503(b)). A married couple can split gifts under IRC §2513 to give $38,000 per recipient per year. Direct payments for tuition and medical expenses (IRC §2503(e)) are unlimited and not counted against the exclusion.

Common high-net-worth strategies include SLATs, GRATs, QPRTs, ILITs, charitable remainder and lead trusts, generation-skipping trusts, family limited partnerships, and A-B (bypass) trusts. For detailed coverage of each strategy, see our California Estate Tax Planning Guide.

Related Resources

California Estate Tax Planning Guide for High-Net-Worth Families: Our pillar resource on SLATs, GRATs, ILITs, charitable trusts, GST trusts, and other strategies for estates approaching or above the federal exemption.

California Trusts: Complete Guide: Trust types, selection criteria, and how each fits into a California estate plan.

California Revocable Living Trust Tax Guide: Tax mechanics specific to revocable living trusts in California, including step-up in basis at death.

Talk to an Experienced California Estate Planning Attorney

Owen Rassman is the Managing Partner of Opelon LLP and holds an LL.M. in Taxation from the University of San Diego School of Law. In his practice with San Diego County families, he has designed more than 700 California estate plans.

To discuss whether the federal exemption affects your planning, schedule a consultation with the team at Opelon LLP.

- Phone: (760) 278-1116

- Email: info@opelon.com

- Office: 1901 Camino Vida Roble STE 112, Carlsbad, CA 92008